Running a business can be extremely rewarding but it is a complex, challenging and demanding engagement. Whether you’re a small startup or a well-established company, there comes a time when you need financial help to keep the business ball rolling. This is where a business loan steps in. What is a business loan? In simple terms, it’s a financial leverage that helps businesses meet their monetary requirements. Be it scaling operations, purchasing new equipment, or managing working capital—business loans are a lifeline for enterprises of all sizes.

In this article, we’ll explore what is a business loan, the different types of loans available in India, and everything you need to know about eligibility and benefits. Let’s dive right in!

What is a Business Loan?

A business loan is a financial solution designed specifically for companies to borrow money for their business needs. Unlike personal loans, which cater to individual requirements, it is focused on helping businesses grow, sustain, and thrive.

For instance, if a retail store owner wants to expand by opening a new outlet, they might apply for commercial financing to cover expenses like rent, inventory, and staffing. Commercial loans can be tailored to suit various needs, whether it’s a one-time purchase or ongoing operational costs.

In simple words, commercial financing is a financial agreement between a business and a lender, where the lender provides funds with the expectation of repayment, typically with interest.

Why Do Businesses Need Loans?

Every business has unique needs, and loans can be a practical solution in many scenarios. Here are some common reasons why businesses seek loans:

- Starting a Business: Entrepreneurs often need funds to kickstart their ventures.

- Expanding Operations: Scaling up requires capital for new locations, hiring staff, or investing in technology.

- Maintaining Cash Flow: Seasonal fluctuations or delayed payments can impact cash flow, and loans help bridge the gap.

- Purchasing Equipment: From machinery to office infrastructure, loans can finance essential purchases.

- Marketing Campaigns: Launching aggressive marketing campaigns to boost sales often requires extra funds.

Types of Business Loans in India

India’s financial market offers a variety of business loans to cater to the diverse needs of businesses operating at different scales. Here’s a breakdown of the most popular ones:

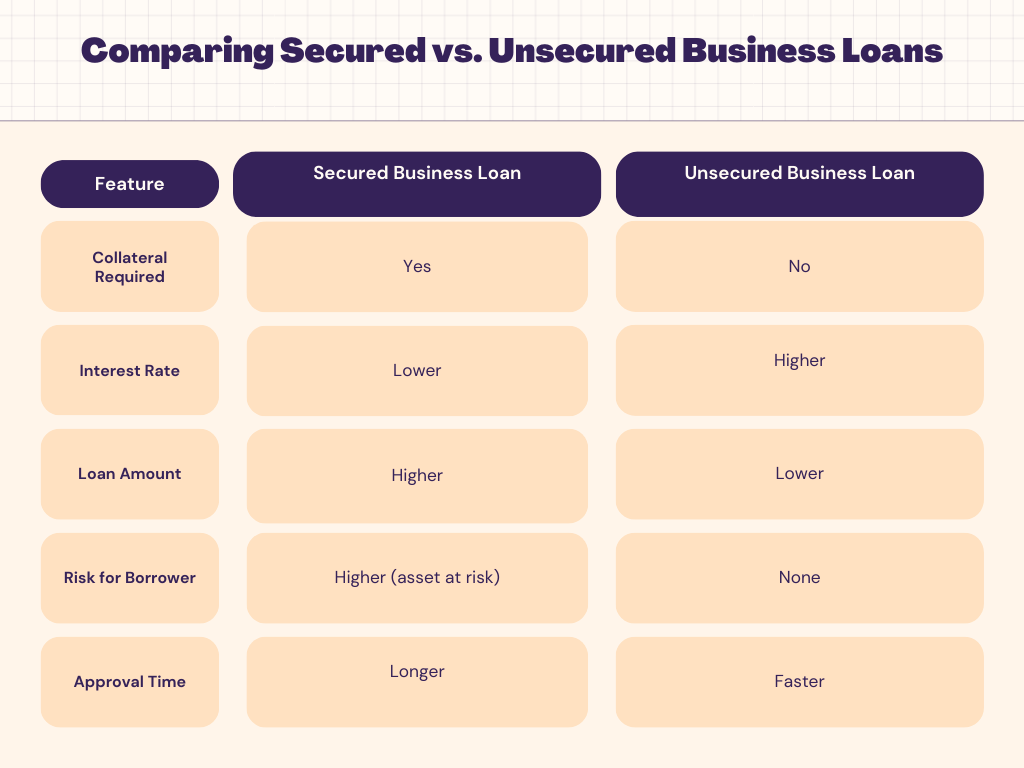

- Secured Business Loans:

These require collateral, such as property, equipment, or inventory. They typically have lower interest rates and higher loan amounts. - Unsecured Business Loans :

No collateral is required, but the interest rates might be higher. These loans are ideal for startups or businesses without significant assets. - Short-term vs. Long-term Loans:

- Short-term loans are great for immediate needs and are repaid within a year.

- Long-term loans are designed for large investments, with repayment periods stretching over several years.

- Overdraft Facilities and Credit Lines:

Flexible borrowing options where businesses can withdraw funds up to a pre-approved limit.

Recommend Read: Types of Business Loans in India You Should Know in 2025

Unsecured Business Loans: An In-Depth Look

Unsecured business loans have gained popularity due to their accessibility. Here’s why they are a game-changer:

- No Collateral Required: Perfect for small businesses or startups without significant assets.

- Quick Processing: Fewer requirements make the approval process faster.

- Flexible Usage: The funds can be used for any business purpose.

Pros:

- Easy to obtain

- No risk of losing collateral

Cons:

- Higher interest rates

- Smaller loan amounts compared to secured loans

Recommend Read: Business Loans vs. Venture Capital: Which is Right for Your Business?

Who is Eligible for a Business Loan?

To secure a business loans, you need to meet certain eligibility criteria. Although the specifics vary by lender, here are the general requirements:

- Age: Applicants should typically be between 21 and 65 years.

- Business Tenure: Most lenders prefer businesses operating for at least 2-3 years.

- Credit Score: A good credit score (usually 650 or above) improves your chances.

- Revenue: Consistent income and financial stability are key factors.

Documentation Required:

- Business registration certificates

- PAN card and Aadhaar card

- Bank statements (6-12 months)

- Income tax returns

- Financial statements (P&L and balance sheet)

How to Apply for a Business Loan in India

Applying for a business loan in India is straightforward if you follow the correct steps. Here’s a step-by-step guide:

- Assess Your Needs:

Determine the loan amount and purpose. Are you financing equipment, boosting working capital, or starting a new project? Clear goals help you choose the right type of loan. - Research Lenders:

Compare offerings from banks, NBFCs (Non-Banking Financial Companies), and online lenders. Focus on interest rates, tenure, and customer reviews. - Check Eligibility Criteria:

Review the specific requirements of your chosen lender. Make sure your business meets their standards for revenue, credit score, and documentation. - Prepare Documents:

Gather all necessary documents such as financial statements, tax returns, and bank statements. - Submit Application:

Fill out the application form with accurate details and attach the required documents. - Loan Approval and Disbursement:

If approved, the lender will issue the loan agreement. Once signed, the funds are transferred to your account.

Documents Required for Business Loans

Having your documents in order can speed up the application process. Here’s what you typically need:

- Business Identity Proof: PAN card, GST registration, or business license.

- Address Proof: Utility bills, lease agreements, or property tax receipts.

- Financial Records: Bank statements, balance sheets, and profit & loss statements.

- KYC Documents: Aadhaar card, PAN card, passport, or voter ID.

- Income Tax Returns: Usually for the last 2-3 years.

Benefits of Business Loans

Taking a Business capital offers numerous advantages, including:

- Growth Opportunities:

Business loans enable you to seize growth opportunities, such as launching new products or expanding your market reach. - Cash Flow Management:

Loans help businesses maintain a steady cash flow, even during slow seasons or when dealing with delayed payments. - Flexible Repayment Options:

Many lenders offer customized repayment schedules to suit your cash flow patterns. - Tax Benefits:

Interest paid on business loans is often tax-deductible, reducing your financial burden. - Preservation of Ownership:

Unlike equity funding, loans allow you to retain full control of your business.

Challenges in Getting a Business Loan

While business loans are highly beneficial, getting one isn’t always easy and simple. Here are some challenges that you might face:

- Strict Eligibility Requirements:

Lenders often require a good credit score, stable income, and several years in business. - Collateral Needs:

Secured loans demand valuable assets as collateral, which may not be feasible for all businesses. - High Interest Rates:

Unsecured loans, while collateral-free, come with higher interest rates that can strain your finances. - Lengthy Processing Times:

Traditional lenders like banks may have slow processing and approval timelines.

What to Do If Your Loan Application is Rejected ?

Benefits of Secured Versus Unsecured Loans

When choosing between secured and unsecured loans, consider the following:

Choose secured loans for larger investments and unsecured loans for smaller, immediate needs.

Top Banks and Institutions Offering Business Loans in India

India is home to numerous banks and other financial institutions offering funds for the business. Here are some top options:

- State Bank of India (SBI):

Offers collateral-free loans under the CGTMSE scheme for SMEs. - HDFC Bank:

Known for quick approval processes and attractive interest rates. - ICICI Bank:

Provides both secured and unsecured loan options with flexible tenures. - Bajaj Finserv:

Offers easy-to-apply unsecured loans for SMEs and startups. - Bank of Baroda:

Ideal for working capital loans and term loans.

Recommend Read:How to Secure a Government Business Loan for Your Startup in India

Maximizing Your Loan Approval Odds

Want to improve your chances of loan approval? Follow these tips:

- Maintain a High Credit Score:

A credit score above 650 significantly boosts your chances of approval. - Show Strong Financial Statements:

Lenders want to see consistent revenue and profitability. - Provide a Detailed Business Plan:

Outline how you’ll use the loan and your repayment strategy. - Opt for a Smaller Loan Amount:

Start with a manageable amount to build credibility with lenders. - Establish Relationships with Lenders:

A good relationship with your bank or any other financial services company can lead to better terms and faster approvals.

Conclusion

Understanding what a business loan is the first step toward making informed financial decisions for your business. Whether you’re expanding operations, stabilizing cash flow, or funding a startup, Financial aid for a business offer invaluable support for driving growth. From secured and unsecured loans to flexible repayment options, the choices are vast. Just ensure you meet the eligibility criteria, prepare your documents, and choose the right Bank, NBFC or Fintech lender to set yourself up for success.

Remember, a Business funding is not just a debt—it’s an investment in your future. So go ahead, explore your options, and make the most of the opportunities ahead.

FAQs

- What is a business loan, and how is it different from a personal loan?

A business loan is a financial solution for business needs, whereas personal loans cater to individual expenses. - What are the types of business loans in India?

Business loans in India include secured loans, unsecured loans, short-term loans, long-term loans, and credit lines. - Who is eligible for a business loan?

Business owners meeting age, credit score, and revenue criteria, with proper documentation, are eligible. - What is an unsecured business loan?

An unsecured business loan requires no collateral and is ideal for small businesses or startups. - How can I improve my chances of getting a business loan?

Maintain a good credit score, provide detailed financial records, and choose the right loan product.