Taking out a loan can feel overwhelming, especially when you’re bombarded with unfamiliar terms and numbers. Whether you’re borrowing for a home, a car, or personal expenses, understanding loan terms is essential to making smart financial decisions. In today’s economic landscape, grasping key concepts like APR, interest rates, and repayment schedules can save you money and prevent financial stress in the long run. So, let’s explore loan terms and focus on understanding APR and interest rates.

What you need to know before borrowing

Understanding loan terms will help you evaluate loan offers and avoid costly surprises. Having loan terms explained clearly is crucial for making informed financial decisions. Let’s start by breaking down some common loan terms.

1. Annual Percentage Rate (APR) vs. Interest Rate

These two terms are often confused but are quite different. Understanding APR and interest rates is crucial when comparing loans:

- Interest Rate: This is the cost of borrowing, expressed as a percentage of the loan amount. If you borrow Rs 10,00,000 at a 5% interest rate, you’ll pay Rs 50,000 in interest over a year.

- APR (Annual Percentage Rate): The APR includes the interest rate and additional costs, such as loan fees or insurance. It gives you a better picture of the total cost of the loan. For example, if the above-mentioned loan also had Rs 10,000 in fees, the APR might be closer to 6%.

Always look at the APR, not just the interest rate, when comparing loans. A lower interest rate could still be more expensive if the APR is higher due to hidden fees.

2. How interest rates are determined

Your loan’s interest rate depends on several factors:

- Credit Score: The higher your score, the lower your interest rate is likely to be.

- Loan Type: Secured loans (like mortgages or car loans) generally have lower interest rates than unsecured loans (like personal loans or credit cards).

- Market Conditions: Economic factors, such as inflation or central bank rates, also influence interest rates.

Understanding what affects interest rates helps you take steps to get the best rate, like improving your credit score or shopping during a low-interest-rate environment. This is a key aspect of understanding APR and interest rates.

3. Principal and Term Length

- Principal: This is the original amount of money you borrowed. For example, if you take out a Rs 15,00,000 loan, that’s your principal.

- Term Length: This is how long you have to repay the loan. A mortgage might have a 30-year term, while a car loan might be for 5 years.

The longer the term, the lower your monthly payments—but the more interest you’ll pay over time. A shorter term will cost less in interest but have higher monthly payments.

4. Loan Fees

Some loans come with additional fees, such as:

- Origination Fees: These are upfront costs for processing the loan, typically 1% to 6% of the loan amount.

- Late Fees: Penalties for missing a payment or paying late.

- Prepayment Penalties: Some loans charge you a fee if you pay off the loan early.

Hidden fees can add up, so make sure you know all the costs before signing any agreement.

Types of repayment schedules

There are different ways you might be required to repay a loan. Let’s go over the most common types as part of our loan terms explained guide.

1. Fixed Monthly Payments

With this option, you make the same payment every month. Mortgages and car loans typically have fixed monthly payments. It’s predictable, and you always know how much to budget.

Pros: Predictability and easier to budget.

Cons: May come with a longer loan term, which can mean more interest paid over time.

2. Variable Payments

Some loans, like adjustable-rate mortgages or credit cards, have payments that change based on the interest rate. If interest rates go up, so do your payments.

Pros: Could save money if interest rates stay low.

Cons: Payments could increase, making it harder to budget.

3. Interest-Only Payments

For certain loans, you might have the option to make interest-only payments for a set period. This means you’re not reducing the principal during this time, just covering the interest.

Pros: Lower payments during the interest-only period.

Cons: After the interest-only period ends, your payments could increase significantly, and you’ll still owe the full principal.

Also Read: Financial literacy for Gen Z – Essential tips

How to compare loan offers

Now that you’re equipped with essential loan knowledge, here’s a step-by-step guide to comparing loans:

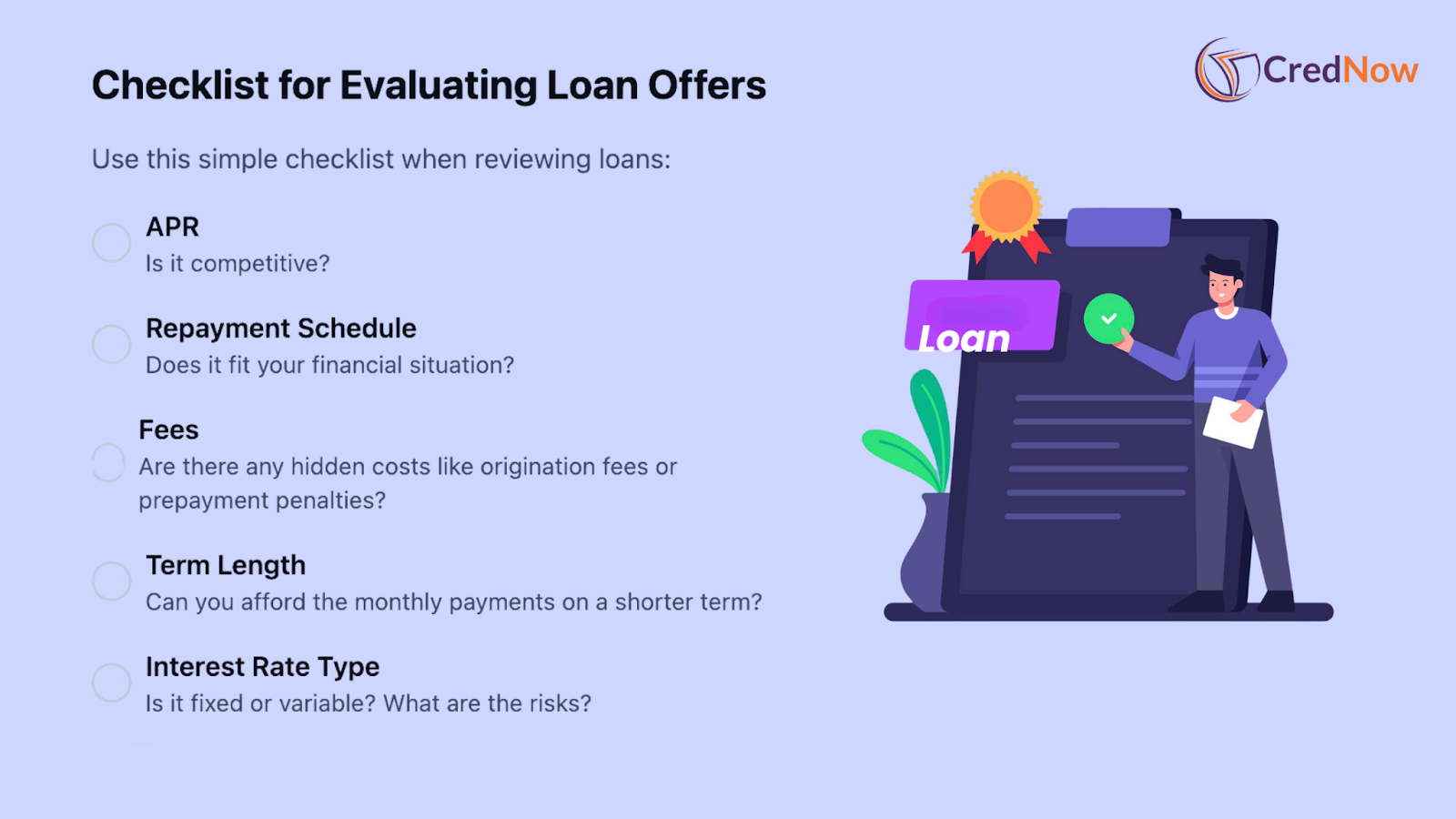

- Compare APRs: Always use the APR as your starting point. This will give you a more accurate picture of the total cost of each loan.

- Check the Repayment Schedule: Does the loan have fixed or variable payments? Which type fits your budget best?

- Review Fees: Make sure you understand all the fees associated with the loan, including any potential prepayment penalties.

- Look at the Loan Term: A longer term means lower monthly payments but more interest over time. Choose the shortest term you can afford.

- Ask Questions: Don’t hesitate to ask the lender for clarification. Make sure you fully understand the loan terms before signing anything.

Real-world example

Let’s say you’re considering two Rs 20,00,000 car loans:

- Loan A: 4% interest rate, 4.5% APR, five-year term, with no fees.

- Loan B: 3.5% interest rate, 5% APR, five-year term, with a Rs 10,000 origination fee.

At first glance, Loan B looks better because of the lower interest rate. But once you factor in the fee, Loan A is actually cheaper overall, even with a slightly higher interest rate.

Glossary of key terms

Here’s a quick reference guide to common loan terms:

- APR (Annual Percentage Rate): The total cost of the loan, including interest and fees.

- Interest Rate: The cost of borrowing money, expressed as a percentage.

- Principal: The original amount you borrow.

- Term Length: The length of time you have to repay the loan.

- Origination Fee: A fee charged for processing the loan.

- Prepayment Penalty: A fee charged if you pay off the loan early.

Checklist for evaluating loan offers

Use this simple checklist when reviewing loans:

Final thoughts

Understanding loan terms is the first step toward making a smart financial decision. Don’t be afraid to ask questions and compare offers carefully before committing. Remember, the right loan for someone else may not be the best for you—always choose a loan that fits your financial goals and budget.

By keeping these tips in mind and focusing on understanding APR and interest rates, you’ll be better equipped to navigate the world of loans with confidence and avoid costly mistakes. Happy borrowing!

FAQs:

1. How are loan terms determined?

Loan terms are influenced by your creditworthiness, the specific lender, and the type of loan product they offer. When you apply for a loan, you’re only eligible for the products and terms provided by that lender. Your credit score and financial situation play a big role in determining which terms (like interest rates and fees) you’re offered.

2. Can I negotiate the terms of my loan?

Yes, loan terms are often negotiable. You can sometimes negotiate lower interest rates or request that certain fees be waived, especially in mortgages or auto loans. Your credit history and overall financial profile may help you get better terms, so it’s always a good idea to ask if improvements can be made.

3. Can I extend my loan term after borrowing?

In some cases, you may be able to extend your loan term. For mortgages, forbearance or refinancing can provide more time for repayment. For personal loans, however, you will need to apply for a new loan, such as through debt consolidation, to restructure the loan term. Keep in mind, that extending the term usually means paying more in interest over time.

4. Are ‘loan terms’ and ‘loan term’ the same thing?

No, they’re different. “Loan terms” refer to the various conditions of the loan, such as interest rates, fees, and repayment schedule. The “loan term,” singular, specifically refers to the period over which you must repay the loan, like a 15-year or 30-year mortgage.

5. What happens if I don’t qualify for favorable loan terms?

If you don’t qualify for the best loan terms due to credit or other factors, you can work on improving your financial situation. Paying off debt, improving your credit score, or providing a larger down payment may help you qualify for better terms in the future, or you could explore refinancing options later to secure more favorable terms.