In the dynamic world of business finance, choosing the right funding option can be crucial for your company’s growth and success. Two popular financing solutions that often compete are line of credit and term loans. While both can inject much-needed capital into your business, they operate differently and cater to distinct financial needs.

Whether you are an established enterprise looking to expand or a startup seeking to manage cash flow, understanding the differences between these two financing options is essential. This blog will explore both options, highlighting their benefits, unique features, and potential drawbacks, guiding you to select the best fit for your business needs.

Understanding a Line of Credit

A line of credit is a flexible financing option that allows businesses to borrow up to a certain limit, as needed, and repay it over time. It operates much like a credit card, offering the flexibility to draw funds up to a specified limit.

Key features of a Line of Credit:

- Flexibility: You can borrow only the amount you need, when you need it, up to the credit limit.

- Interest Rates: Interest is charged only on the borrowed amount, not the entire credit limit.

- Revolving Credit: As you repay the borrowed amount, the credit becomes available again.

- Short-Term Solution: Ideal for managing cash flow fluctuations and short-term financial needs.

Advantages of a Line of Credit:

- Cash Flow Management: Helps businesses manage short-term financial gaps and unexpected expenses.

- Interest Savings: Pay interest only on the funds you use.

- Quick Access to Funds: Once approved, you can access funds whenever required without going through the loan approval process again.

Disadvantages of a Line of Credit:

- Higher Interest Rates: Typically, lines of credit have higher interest rates compared to term loans.

- Variable Rates: Interest rates can fluctuate, making it harder to predict costs.

- Potential for Over-Borrowing: Easy access to funds may lead to excessive borrowing and debt accumulation.

Understanding a Term Loan

A term loan is a lump sum of money borrowed from a lender, which is repaid over a fixed period with regular installments. These loans are often used for long-term investments or capital expenditures.

Key Features of a Term Loan:

- Fixed Amount: Borrow a specific amount based on the business needs.

- Fixed Term: Repayment is spread over a set period, typically ranging from one to ten years.

- Fixed or Variable Interest Rates: Choose between fixed rates (stable payments) or variable rates (potentially lower initial rates).

- Secured or Unsecured: May require collateral depending on the loan amount and lender’s requirements.

Advantages of a Term Loan:

- Predictability: Fixed payments and interest rates provide certainty in financial planning.

- Lower Interest Rates: Often, term loans have lower interest rates compared to lines of credit.

- Suitable for Large Investments: Ideal for funding long-term projects, acquisitions, or capital investments.

Disadvantages of a Term Loan:

- Less Flexibility: The loan amount and repayment schedule are fixed, offering less flexibility than a line of credit.

- Collateral Requirement: Larger loans may require collateral, posing a risk to business assets.

- Long Approval Process: Securing a term loan can be time-consuming due to extensive documentation and credit checks.

Experience CredNow’s Powerful Credit Solutions Today!

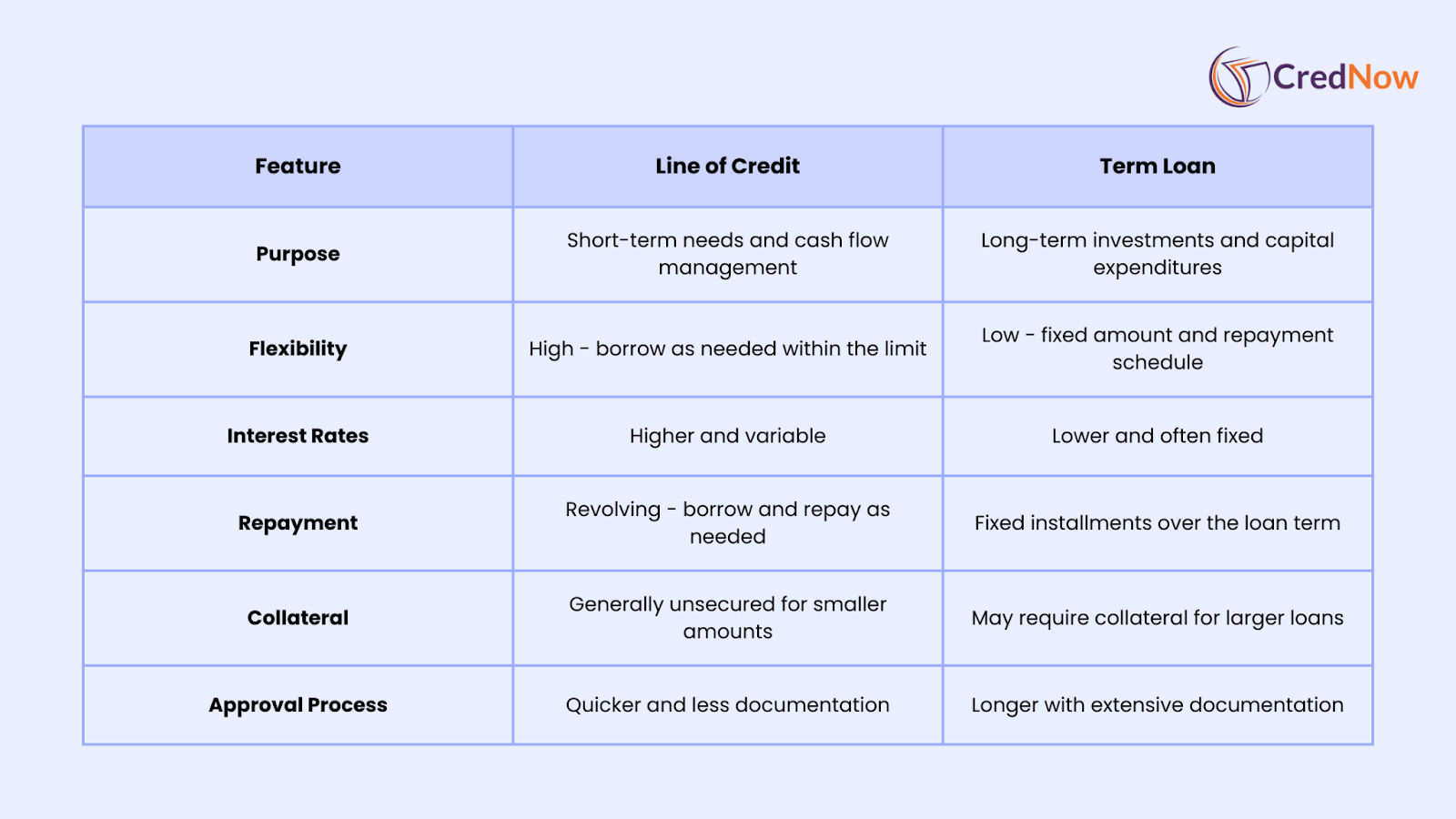

Line of Credit vs. Term Loan: Key differences

To help you choose between a line of credit and a term loan, consider the following key differences:

Must Read: Securing government-backed loans in India

How to choose the right option for your business

When deciding between a line of credit and a term loan, consider the following factors:

1. Business Needs:

- Short-Term Needs: If you need funds for working capital, inventory purchase, or unexpected expenses, a line of credit may be more suitable.

- Long-Term Investments: For expansion, purchasing equipment, or other large investments, a term loan could be the better option.

2. Financial Stability:

- Stable Cash Flow: A stable cash flow can support the fixed repayments of a term loan.

- Variable Cash Flow: A line of credit provides flexibility for businesses with variable income.

3. Interest Rate Preferences:

- Predictable Costs: If you prefer predictable monthly payments, opt for a term loan with fixed interest rates.

- Potential Savings: If you can manage variable rates, a line of credit may offer savings when interest rates are low.

4. Collateral:

- Asset Availability: Consider whether you have assets to offer as collateral for a term loan.

- Risk Tolerance: Evaluate your willingness to risk business assets for a secured loan.

Conclusion

Choosing between a line of credit and a term loan depends on your business’s unique needs, financial situation, and future goals. A line of credit offers flexibility and is ideal for short-term needs, while a term loan provides stability and is suited for long-term investments. By carefully assessing your business requirements and consulting with financial advisors, you can select the best financing option to support your business growth and success in the dynamic Indian market.

FAQs

1. Can I have both a line of credit and a term loan?

Yes, many businesses use both options simultaneously to balance short-term needs and long-term investments.

2. How does a secured loan differ from an unsecured loan?

A secured loan requires collateral, such as property or equipment, whereas an unsecured loan does not. Secured loans typically offer lower interest rates.

3. What happens if I miss a payment on a term loan?

Missing a payment can result in late fees, increased interest rates, and potential damage to your credit score. It’s crucial to communicate with your lender if you anticipate payment difficulties.

4. How is the credit limit determined for a line of credit?

The credit limit is based on the business’s creditworthiness, financial history, and lender’s policies.

5. Which option is better for a startup business?

Startups with unpredictable cash flows might benefit more from a line of credit due to its flexibility. However, for specific capital investments, a term loan may be appropriate if the startup can meet the lender’s requirements.